DISCLAIMER: Any losses incurred based on the content of this post are the responsibility of the trader, not the author. The author takes no responsibility for the conduct of others nor offers any guarantees.

Introduction

You may have noticed I’ve been writing a lot about quantstrat, an R package for developing and backtesting trading strategies. The package strikes me as being so flexible, there’s still more to write about. So far I’ve introduced the package here and here, then recently discussed the important of accounting for transaction costs (and how to do so).

Next up, I want to look at modelling different kinds of orders. The strategy I’ve been looking at so far places orders as they happen. However, traders may desire to place orders such as a stop-loss (to prevent further losses, with the belief that if a stock’s price moves down it will continue to move down, causing further losses), a target price (there should be a target price that, when reached, terminates a trade, locking in gains), and sometimes a trailing stop (if a stock has made gains, better to lock them in at a slightly lower price should a slight reversal be seen than lose all gains in a major reversal). When I took a class on trading, a recommended rule was to have an order representing the target price and a stop-loss order, always. This was mostly to enforce structure and trading discipline, helping take emotions out of the equation. Furthermore, the loss that would result from a stop-loss’s trigger should be half of potential gain, as per the justification that if half the time you “win” and half the time you “lose”, your gains would be twice as large as your losses.

I don’t have nearly enough experience in trading to have a respectable opinion, but what opinion I do have doesn’t look favorably on stop-loss orders as I learned them. I would implement the so-called 2-to-1 rule (that is, target profits are twice maximum losses) in simulations and watch as my orders would be wiped out by large, spurious, immediately corrected movements. It seemed as if reversals would inevitably follow the trigger of the stop-loss that closed my position, locking in losses in addition to transaction costs. I also closely tied, in my mind, the 2-to-1 rule with stop-loss orders in general, and it doesn’t take long to realize the logic of that rule is total bunk. If price movements are a random walk, having a shorter stop-loss means that there’s a good chance the stop-loss would be triggered before the profitable exit order. You might be making twice as much for profitable orders, but you’re triggering the stop-loss twice as often, nullifying the effect (while driving up transaction costs). If you were setting your profit target shorter than the stop-loss, at least more trades would be profits instead of most being losses. (In the random-walk situation it makes no difference; expected profits are zero in either case. But at least it feels better.) I never tried a trailing stop, but I’m sure my opinion would be about the same; “noise” is more likely to close a position than an actual reversal in trend, in my opinion.

I appreciate the call for combating personal psychology, enforcing discipline, having an exit plan and a guard against unacceptably high losses. I’m aware that risk management is an important part of any trading system, and as I write this I am sure that there are better approaches than what I had learned (I hold out hope for VaR assessment, though I have yet to try it out). But I have little love for the approach to stop-losses as I learned it, which is partly why the strategies I’ve looked at so far have closed positions only when the indicators pointed to a change in regime.

That being said, I’m still interested in modelling them. I could be wrong. And more intelligent approaches to risk management likely resemble a simple stop-loss.

I also want to look at parameter optimization with quantstrat. We’ve been using 20-day and 50-day moving averages without questioning what makes those numbers special. quantstrat provides functions that allow for backtesting a strategy while trying out multiple parameters so one can hopefully find a more profitable combination. Now, that said, what I will likely have done is overfit my strategy; the optimal combination looks good in backtesting thanks to torturing the data, but when deployed it will likely perform miserably (or at least not nearly as well as the backtest would suggest). A correction for this should be applied. In the future I may write about how to handle overfitting, but for now, I’m just getting started with the tools.

Adding Stop-Loss Rules

If you’ve been following along with my articles, the next few lines of code should look very familiar, so I won’t repeat the explanation. Let’s just say we’re going to pick up where the article on accounting for transaction costs left off. We’ll work with a \$100,000 trading portfolio that faces \$5 in total for transaction costs per trade. We’ll even tack on an additional 0.1% loss per trade to simulate slippage. We’ll be requiring that trades be done in batches of 100. All told, we end up with the following code (read earlier articles for better explanations):

if (!require("quantstrat")) {

install.packages("quantstrat", repos="http://R-Forge.R-project.org")

library(quantstrat)

}

sigCrossover2 <- function(label, data = mktdata, columns,

relationship = c("gt", "lt", "eq", "gte", "lte"),

offset1 = 0, offset2 = 0) {

# A wrapper for sigCrossover, exhibiting the same behavior except returning

# an object containing TRUE/FALSE instead of TRUE/NA

res <- sigCrossover(label = label, data = data, columns = columns,

relationship = relationship, offset1 = offset1,

offset2 = offset2)

res[is.na(res)] <- FALSE

return(res)

}

# Based on Ilya Kipnis's osMaxDollar(); lots of recycled code

osMaxDollarBatch = function(data, timestamp, orderqty, ordertype, orderside,

portfolio, symbol, prefer = "Open", tradeSize,

maxSize, batchSize = 100, integerQty = TRUE,

...) {

# An order sizing function that limits position size based on dollar value of

# the position, optionally controlling for number of batches to purchase

#

# Args:

# data: ??? (held over from Mr. Kipnis's original osMaxDollar function)

# timestamp: The current date being evaluated (some object, like a string,

# from which time can be inferred)

# orderqty: ??? (held over from Mr. Kipnis's original osMaxDollar function)

# ordertype: ??? (held over from Mr. Kipnis's original osMaxDollar

# function)

# orderside: ??? (held over from Mr. Kipnis's original osMaxDollar

# function)

# portfolio: A string representing the portfolio being treated; will be

# passed to getPosQty

# symbol: A string representing the symbol being traded

# prefer: A string that indicates whether the Open or Closing price is

# used for determining the price of the asset in backtesting (set

# to "Close" to use the closing price)

# tradeSize: Numeric, indicating the dollar value to transact (using

# negative numbers for selling short)

# maxSize: Numeric, indicating the dollar limit to the position (use

# negative numbers for the short side)

# batchSize: The number of stocks purchased per batch (only applies if

# integerQty is TRUE); default value is 100, but setting to 1

# effectively nullifies the batchSize

# integerQty: A boolean indicating whether or not to truncate to the

# nearest integer of contracts/shares/etc.

# ...: ??? (held over from Mr. Kipnis's original osMaxDollar function)

#

# Returns:

# A numeric quantity representing the number of shares to purchase

pos = getPosQty(portfolio, symbol, timestamp)

if (prefer == "Close") {

price = as.numeric(Cl(mktdata[timestamp, ]))

} else {

price = as.numeric(Op(mktdata[timestamp, ]))

}

posVal = pos * price

if (orderside == "short") {

dollarsToTransact = max(tradeSize, maxSize - posVal)

if (dollarsToTransact > 0) {

dollarsToTransact = 0

}

} else {

dollarsToTransact = min(tradeSize, maxSize - posVal)

if (dollarsToTransact < 0) {

dollarsToTransact = 0

}

}

qty = dollarsToTransact/price

if (integerQty) {

# Controlling for batch size only makes sense if we were working with

# integer quantities anyway; if we didn't care about being integers,

# why bother?

qty = trunc(qty / batchSize) * batchSize

}

return(qty)

}

fee <- function(TxnQty, TxnPrice, Symbol) {

# A function for computing a transaction fee that is 2% of total value of

# transaction

#

# Args:

# TxnQty: Numeric for number of shares being traded

# TxnPrice: Numeric for price per share

# Symbol: The symbol being traded (not used here, but will be passed)

#

# Returns:

# The fee to be applied

return(-0.001 * abs(TxnQty * TxnPrice) - 5)

}

start <- as.Date("2010-01-01")

end <- as.Date("2016-10-01")

rm(list = ls(.blotter), envir = .blotter) # Clear blotter environment

currency("USD") # Currency being used

Sys.setenv(TZ = "MDT") # Allows quantstrat to use timestamps

initDate <- "2009-12-31" # A date prior to first close price; needed (why?)

# Get new symbols

symbols <- c("AAPL", "MSFT", "GOOG", "FB", "TWTR", "NFLX", "AMZN", "YHOO",

"SNY", "NTDOY", "IBM", "HPQ")

getSymbols(Symbols = symbols, src = "yahoo", from = start, to = end,

adjust = TRUE) # The last argument tells getSymbols to use adjusted

# prices

stock(symbols, currency = "USD", multiplier = 1)

strategy_st <- "SMAC-20-50_STRAT"

portfolio_st <- "SMAC-20-50_PORTF"

account_st <- "SMAC-20-50_ACCT"

rm.strat(portfolio_st)

rm.strat(strategy_st)

initPortf(portfolio_st, symbols = symbols,

initDate = initDate, currency = "USD")

initAcct(account_st, portfolios = portfolio_st,

initDate = initDate, currency = "USD",

initEq = 100000)

initOrders(portfolio_st, store = TRUE)

strategy(strategy_st, store = TRUE)

add.indicator(strategy = strategy_st, name = "SMA",

arguments = list(x = quote(Cl(mktdata)),

n = 20),

label = "fastMA")

add.indicator(strategy = strategy_st, name = "SMA",

arguments = list(x = quote(Cl(mktdata)),

n = 50),

label = "slowMA")

add.signal(strategy = strategy_st, name = "sigCrossover2", # Remember me?

arguments = list(columns = c("fastMA", "slowMA"),

relationship = "gt"),

label = "bull")

add.signal(strategy = strategy_st, name = "sigCrossover2",

arguments = list(columns = c("fastMA", "slowMA"),

relationship = "lt"),

label = "bear")

Now I add the stop-loss order. This is done by adding a new rule. First, note that I start by adding the same rules I had before. Then, I add a rule labeled stop_loss (the name of the label has no special meaning; it’s useful to the programmer, not to blotter) with order type "stoplimit" that

add.rule(strategy = strategy_st, name = "ruleSignal",

arguments = list(sigcol = "bull",

sigval = TRUE,

ordertype = "market",

orderside = "long",

replace = FALSE,

TxnFees = "fee",

prefer = "Open",

osFUN = osMaxDollarBatch,

maxSize = quote(floor(getEndEq(account_st,

Date = timestamp) * .1)),

tradeSize = quote(floor(getEndEq(account_st,

Date = timestamp) * .1)),

batchSize = 100),

type = "enter", path.dep = TRUE, label = "buy")

add.rule(strategy = strategy_st, name = "ruleSignal",

arguments = list(sigcol = "bear",

sigval = TRUE,

orderqty = "all",

ordertype = "market",

orderside = "long",

replace = FALSE,

TxnFees = "fee",

prefer = "Open"),

type = "exit", path.dep = TRUE, label = "sell")

# Now for setting a stop-loss

add.rule(strategy = strategy_st, name = "ruleSignal",

arguments = list(sigcol = "bull",

sigval = TRUE,

replace = FALSE,

orderside = "long",

TxnFees = "fee",

# Now we set up a stop-limit order

ordertype = "stoplimit", # Order type is stop-limit

orderqty = "all", # Clear all stocks

#osFUN = osMaxPos, # Clear ALL stocks

tmult = TRUE, # Forces threshold to be a percent

# multiplier of the price

threshold = 0.01), # With tmult set to TRUE, we are

# saying, in effect, that if the

# price drops below 1% of what it

# was when we opened the position

# then sell all stocks to close

# the position

type = "chain", parent = "buy", label = "stop_loss")

# Having set up the strategy, we now backtest

applyStrategy(strategy_st, portfolios = portfolio_st)

Let’s now look at the results:

updatePortf(portfolio_st)

dateRange <- time(getPortfolio(portfolio_st)$summary)[-1]

updateAcct(account_st, dateRange)

updateEndEq(account_st)

tStats <- tradeStats(Portfolios = portfolio_st, use="trades",

inclZeroDays = FALSE)

tStats[, 4:ncol(tStats)] <- round(tStats[, 4:ncol(tStats)], 2)

print(data.frame(t(tStats[, -c(1,2)])))

## AAPL FB HPQ MSFT NFLX NTDOY ## Num.Txns 29.00 20.00 30.00 40.00 30.00 38.00 ## Num.Trades 15.00 10.00 15.00 20.00 15.00 19.00 ## Net.Trading.PL 4298.51 -2422.29 -1588.25 646.16 1049.23 -2548.65 ## Avg.Trade.PL 311.17 -216.36 -77.40 59.31 96.16 -106.86 ## Med.Trade.PL -73.68 -155.00 -93.94 -89.85 -70.24 -100.31 ## Largest.Winner 2226.34 0.00 457.03 1730.06 2227.61 975.16 ## Largest.Loser -182.85 -506.09 -366.77 -236.43 -411.43 -581.40 ## Gross.Profits 5676.98 0.00 471.52 2827.93 2814.00 1067.00 ## Gross.Losses -1009.48 -2163.57 -1632.49 -1641.79 -1371.53 -3097.30 ## Std.Dev.Trade.PL 813.66 170.03 166.41 470.98 620.71 318.32 ## Percent.Positive 26.67 0.00 6.67 15.00 20.00 10.53 ## Percent.Negative 73.33 100.00 93.33 85.00 80.00 89.47 ## Profit.Factor 5.62 0.00 0.29 1.72 2.05 0.34 ## Avg.Win.Trade 1419.24 NaN 471.52 942.64 938.00 533.50 ## Med.Win.Trade 1672.59 NA 471.52 1025.28 486.86 533.50 ## Avg.Losing.Trade -91.77 -216.36 -116.61 -96.58 -114.29 -182.19 ## Med.Losing.Trade -74.72 -155.00 -94.03 -92.06 -86.53 -105.00 ## Avg.Daily.PL 200.98 -229.18 -91.60 45.78 83.01 -120.45 ## Med.Daily.PL -86.29 -168.91 -108.24 -103.75 -82.19 -115.24 ## Std.Dev.Daily.PL 747.88 170.59 166.30 470.24 619.83 317.84 ## Ann.Sharpe 4.27 -21.33 -8.74 1.55 2.13 -6.02 ## Max.Drawdown -1213.74 -2438.98 -2089.63 -1262.90 -2406.00 -5441.27 ## Profit.To.Max.Draw 3.54 -0.99 -0.76 0.51 0.44 -0.47 ## Avg.WinLoss.Ratio 15.47 NaN 4.04 9.76 8.21 2.93 ## Med.WinLoss.Ratio 22.38 NA 5.01 11.14 5.63 5.08 ## Max.Equity 4550.51 0.00 501.38 1828.40 3091.81 2892.62 ## Min.Equity -588.23 -2438.98 -1588.25 -892.32 -672.04 -2548.65 ## End.Equity 4298.51 -2422.29 -1588.25 646.16 1049.23 -2548.65 ## SNY TWTR YHOO ## Num.Txns 44.00 10.00 44.00 ## Num.Trades 22.00 5.00 22.00 ## Net.Trading.PL -2580.59 -812.73 -1687.53 ## Avg.Trade.PL -89.88 -135.57 -49.90 ## Med.Trade.PL -108.91 -88.38 -93.06 ## Largest.Winner 771.70 0.00 1119.31 ## Largest.Loser -622.70 -348.17 -242.21 ## Gross.Profits 1016.64 0.00 1134.00 ## Gross.Losses -2993.91 -677.84 -2231.74 ## Std.Dev.Trade.PL 240.15 111.79 267.78 ## Percent.Positive 13.64 0.00 4.55 ## Percent.Negative 86.36 100.00 95.45 ## Profit.Factor 0.34 0.00 0.51 ## Avg.Win.Trade 338.88 NaN 1134.00 ## Med.Win.Trade 145.86 NA 1134.00 ## Avg.Losing.Trade -157.57 -135.57 -106.27 ## Med.Losing.Trade -137.44 -88.38 -93.48 ## Avg.Daily.PL -103.54 -148.99 -63.28 ## Med.Daily.PL -123.11 -102.13 -107.27 ## Std.Dev.Daily.PL 240.26 111.71 267.52 ## Ann.Sharpe -6.84 -21.17 -3.75 ## Max.Drawdown -3061.63 -3726.33 -3225.56 ## Profit.To.Max.Draw -0.84 -0.22 -0.52 ## Avg.WinLoss.Ratio 2.15 NaN 10.67 ## Med.WinLoss.Ratio 1.06 NA 12.13 ## Max.Equity 472.26 2913.60 1538.03 ## Min.Equity -2589.37 -812.73 -1687.53 ## End.Equity -2580.59 -812.73 -1687.53

final_acct <- getAccount(account_st) plot(final_acct$summary$End.Eq["2010/2016"], main = "Portfolio Equity")

Eesh. Not good. The fees were not helping, but they’re relatively small in this context, so the effect we see is likely thanks to the stop-loss orders. Positions are getting closed out before being given a chance to be profitable, locking in losses.

As mentioned before, there may be a better way to pick the stop-loss than simply saying, “if the value drops below 1%, exit the position.” I won’t discuss this now.

But let’s turn this awful rule off, and see what happens when we don’t use this stop-loss (you’ve now seen a new rule in the toolbox, enable.rule()):

# Disable the stop-loss rule

enable.rule(strategy_st, type = "chain", label = "stop_loss", enabled = FALSE)

# Clear the portfolio and account, and start over

rm.strat(portfolio_st)

rm.strat(account_st)

initPortf(portfolio_st, symbols = symbols,

initDate = initDate, currency = "USD")

initAcct(account_st, portfolios = portfolio_st,

initDate = initDate, currency = "USD",

initEq = 100000)

initOrders(portfolio_st, store = TRUE)

# Retry the strategy

applyStrategy(strategy_st, portfolios = portfolio_st)

updatePortf(portfolio_st)

dateRange <- time(getPortfolio(portfolio_st)$summary)[-1]

updateAcct(account_st, dateRange)

updateEndEq(account_st)

tStats <- tradeStats(Portfolios = portfolio_st, use="trades",

inclZeroDays = FALSE)

tStats[, 4:ncol(tStats)] <- round(tStats[, 4:ncol(tStats)], 2)

print(data.frame(t(tStats[, -c(1,2)])))

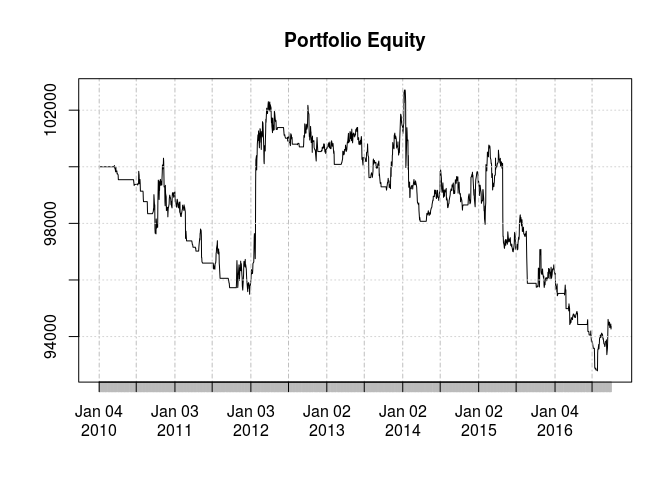

## AAPL FB HPQ MSFT NFLX NTDOY ## Num.Txns 29.00 20.00 29.00 39.00 29.00 37.00 ## Num.Trades 15.00 10.00 15.00 20.00 15.00 19.00 ## Net.Trading.PL 7696.42 8232.62 4731.16 1954.50 21583.36 1836.17 ## Avg.Trade.PL 537.92 850.20 343.26 124.25 1465.49 123.37 ## Med.Trade.PL 167.09 509.00 -82.40 -203.68 250.00 -140.00 ## Largest.Winner 2226.34 6052.90 4974.94 1730.06 14571.00 4264.69 ## Largest.Loser -550.58 -1485.24 -1433.67 -1046.06 -2746.44 -785.14 ## Gross.Profits 9450.71 10682.00 11623.43 7785.50 26293.29 7485.00 ## Gross.Losses -1381.90 -2180.00 -6474.56 -5300.49 -4311.00 -5141.00 ## Std.Dev.Trade.PL 895.23 2025.78 1917.71 792.77 3965.07 1157.29 ## Percent.Positive 60.00 70.00 40.00 45.00 66.67 42.11 ## Percent.Negative 40.00 30.00 60.00 55.00 33.33 57.89 ## Profit.Factor 6.84 4.90 1.80 1.47 6.10 1.46 ## Avg.Win.Trade 1050.08 1526.00 1937.24 865.06 2629.33 935.62 ## Med.Win.Trade 928.68 881.00 965.61 772.12 1088.36 240.00 ## Avg.Losing.Trade -230.32 -726.67 -719.40 -481.86 -862.20 -467.36 ## Med.Losing.Trade -144.28 -432.00 -822.36 -426.43 -355.71 -540.00 ## Avg.Daily.PL 443.68 836.31 248.98 96.08 1537.80 40.63 ## Med.Daily.PL 116.79 496.63 -291.88 -244.54 223.41 -161.50 ## Std.Dev.Daily.PL 869.23 2023.81 1962.03 810.87 4095.34 1148.46 ## Ann.Sharpe 8.10 6.56 2.01 1.88 5.96 0.56 ## Max.Drawdown -1380.74 -3840.91 -5105.22 -2847.65 -5136.97 -4923.73 ## Profit.To.Max.Draw 5.57 2.14 0.93 0.69 4.20 0.37 ## Avg.WinLoss.Ratio 4.56 2.10 2.69 1.80 3.05 2.00 ## Med.WinLoss.Ratio 6.44 2.04 1.17 1.81 3.06 0.44 ## Max.Equity 7948.42 8859.91 4990.56 3363.71 24293.63 4104.90 ## Min.Equity -852.19 -1349.93 -5105.22 -1915.50 -321.11 -3042.10 ## End.Equity 7696.42 8232.62 4731.16 1954.50 21583.36 1836.17 ## SNY TWTR YHOO ## Num.Txns 44.00 9.00 43.00 ## Num.Trades 22.00 5.00 22.00 ## Net.Trading.PL -2804.64 2672.47 8541.60 ## Avg.Trade.PL -100.07 558.40 414.91 ## Med.Trade.PL 32.83 -2.00 -111.00 ## Largest.Winner 1423.13 136.69 5278.10 ## Largest.Loser -1638.89 -954.90 -623.00 ## Gross.Profits 5610.84 4236.00 13265.00 ## Gross.Losses -7812.38 -1444.00 -4137.00 ## Std.Dev.Trade.PL 781.97 2018.43 1370.80 ## Percent.Positive 54.55 40.00 31.82 ## Percent.Negative 45.45 60.00 68.18 ## Profit.Factor 0.72 2.93 3.21 ## Avg.Win.Trade 467.57 2118.00 1895.00 ## Med.Win.Trade 293.30 2118.00 1134.00 ## Avg.Losing.Trade -781.24 -481.33 -275.80 ## Med.Losing.Trade -669.52 -500.00 -258.00 ## Avg.Daily.PL -113.73 -336.44 369.19 ## Med.Daily.PL 19.11 -263.77 -128.76 ## Std.Dev.Daily.PL 781.34 497.04 1394.80 ## Ann.Sharpe -2.31 -10.75 4.20 ## Max.Drawdown -3471.19 -4840.52 -2825.76 ## Profit.To.Max.Draw -0.81 0.55 3.02 ## Avg.WinLoss.Ratio 0.60 4.40 6.87 ## Med.WinLoss.Ratio 0.44 4.24 4.40 ## Max.Equity 666.55 3144.99 8863.60 ## Min.Equity -3249.87 -1695.53 -1302.96 ## End.Equity -2804.64 2672.47 8541.60

final_acct <- getAccount(account_st) plot(final_acct$summary$End.Eq["2010/2016"], main = "Portfolio Equity")

That’s much better.

Parameter Optimization

What makes a 20-day moving average special? What about a 50-day moving average? These numbers were chosen arbitrarily, so there’s no reason to believe that they will produce the best results. So how about we try different combinations of windows for the moving averages used in the moving averace crossover strategy, and pick the combination that obtains the best results?

quantstrat easily implements this behavior. We can keep the strategy we’ve already defined, but we will be varying the parameters used in the moving averages, ‘n’ in particular. This can be accomplished by adding a distribution to the parameters of interest in the strategy, via the function add.distribution().

# Possible windows for the fast moving average

add.distribution(strategy_st, # The strategy being optimized

paramset.label = "MA", # Some label to identify the parameter

# set being optimized

component.type = "indicator", # The component type we're

# optimizing, in this case an

# indicator

component.label = "fastMA", # The name of the indicator we

# are optimizing

variable = list(n = 5 * 1:10), # A list with the name of the

# variable we are optimizing

# along with a vector of

# allowed values

label = "nFAST") # The label for the distribution

# Possible windows for the slow moving average

add.distribution(strategy_st, paramset.label = "MA",

component.type = "indicator", component.label = "slowMA",

variable = list(n = 25 * 1:10), label = "nSLOW")

We need to add a constraint to the parameter values since we do not want the window size of the fast moving average to exceed the window size of the slow moving average; this would not make sense. This constraint can be added via add.distribution.constraint():

add.distribution.constraint(strategy_st, # The name of strategy to apply the

# constraint to

paramset.label = "MA", # The name of the parameter

# set (which was defined

# when we created the

# distributions) containing

# the parameters being

# optimized

distribution.label.1 = "nFAST", # First parameter

# involved in the

# constraint

distribution.label.2 = "nSLOW", # Second parameter

operator = "<", # The operator for the relation

# that defines the constraint;

# translate this to mean,

# nFAST < nSLOW

label = "MA.Constraint") # The label for the

# constraint

Having given distributions, we now optimize. The function apply.paramset() repeatedly applies the strategy with different combinations of the parameters in the parameter set. The parameter nsamples controls how many combinations to try, and the combinations actually chosen are random (and presumably don’t repeat). If this is zero, all combinations will be chosen. This is fine if there are few parameters to try, but otherwise, beware; the time spent trying out different combinations could explode.

This step is naturally computationally intense. A single backtest can take some time, so just imagine how much time it would take to complete 40! One way to speed up the process is to parallellize it. quantstrat supports parallellization, and implementing it is as simple as loading the package doParallel and registering cores to be used in the parallelization; apply.paramset() already uses %dopar% and foreach() from the foreach package. I don’t show this here, just because there would be no advantage to it with the system I’m currently using.

We will try 40 different combinations here.

set.seed(2017052319) # Set seed for reproducibility

results <- apply.paramset(strategy_st, # Strategy to optimize

paramset.label = "MA", # The parameter set to

# optimize

portfolio.st = portfolio_st, # The portfolio to use;

# copies will be made

# in the blotter

# environment with

# their own names so

# their statistics can

# be analyzed

account.st = account_st, # The name of the account

# to initialize with

nsamples = 40) # The number of combinations of

# parameters to try

results is a list containing some summary statistics for each backtest performed. Below I show its structure:

# Global view of the list names(results)

## [1] "SMAC-20-50_PORTF.5" "tradeStats" "SMAC-20-50_PORTF.14" ## [4] "SMAC-20-50_PORTF.34" "SMAC-20-50_PORTF.35" "SMAC-20-50_PORTF.55" ## [7] "SMAC-20-50_PORTF.85" "SMAC-20-50_PORTF.3" "SMAC-20-50_PORTF.26" ## [10] "SMAC-20-50_PORTF.56" "SMAC-20-50_PORTF.66" "SMAC-20-50_PORTF.76" ## [13] "SMAC-20-50_PORTF.8" "SMAC-20-50_PORTF.37" "SMAC-20-50_PORTF.67" ## [16] "SMAC-20-50_PORTF.87" "SMAC-20-50_PORTF.28" "SMAC-20-50_PORTF.58" ## [19] "SMAC-20-50_PORTF.78" "SMAC-20-50_PORTF.88" "SMAC-20-50_PORTF.10" ## [22] "SMAC-20-50_PORTF.19" "SMAC-20-50_PORTF.29" "SMAC-20-50_PORTF.59" ## [25] "SMAC-20-50_PORTF.79" "SMAC-20-50_PORTF.60" "SMAC-20-50_PORTF.80" ## [28] "SMAC-20-50_PORTF.90" "SMAC-20-50_PORTF.21" "SMAC-20-50_PORTF.31" ## [31] "SMAC-20-50_PORTF.41" "SMAC-20-50_PORTF.61" "SMAC-20-50_PORTF.71" ## [34] "SMAC-20-50_PORTF.13" "SMAC-20-50_PORTF.32" "SMAC-20-50_PORTF.92" ## [37] "SMAC-20-50_PORTF.33" "SMAC-20-50_PORTF.43" "SMAC-20-50_PORTF.73" ## [40] "SMAC-20-50_PORTF.83" "SMAC-20-50_PORTF.93"

# Seeing the structure of one element str(results[[10]])

## List of 3 ## $ param.combo :'data.frame': 1 obs. of 2 variables: ## ..$ nFAST: num 15 ## ..$ nSLOW: num 175 ## ..- attr(*, "out.attrs")=List of 2 ## .. ..$ dim : Named int [1:2] 10 10 ## .. .. ..- attr(*, "names")= chr [1:2] "nFAST" "nSLOW" ## .. ..$ dimnames:List of 2 ## .. .. ..$ nFAST: chr [1:10] "nFAST= 5" "nFAST=10" "nFAST=15" "nFAST=20" ... ## .. .. ..$ nSLOW: chr [1:10] "nSLOW= 25" "nSLOW= 50" "nSLOW= 75" "nSLOW=100" ... ## $ portfolio.st: chr "SMAC-20-50_PORTF.56" ## $ tradeStats :'data.frame': 8 obs. of 30 variables: ## ..$ Portfolio : Factor w/ 1 level "SMAC-20-50_PORTF.56": 1 1 1 1 1 1 1 1 ## ..$ Symbol : Factor w/ 8 levels "AAPL","HPQ","MSFT",..: 1 2 3 4 5 6 7 8 ## ..$ Num.Txns : num [1:8] 7 13 19 7 17 26 5 15 ## ..$ Num.Trades : int [1:8] 3 6 9 3 8 13 2 7 ## ..$ Net.Trading.PL : num [1:8] 13829 7186 5425 33271 -1341 ... ## ..$ Avg.Trade.PL : num [1:8] 4382 715 577 11134 -433 ... ## ..$ Med.Trade.PL : num [1:8] 4921 -970 -436 5894 -905 ... ## ..$ Largest.Winner : num [1:8] 9399 5370 5663 28419 3965 ... ## ..$ Largest.Loser : num [1:8] -1174 -1848 -912 -910 -2037 ... ## ..$ Gross.Profits : num [1:8] 14321 9250 8748 34313 3988 ... ## ..$ Gross.Losses : num [1:8] -1174 -4960 -3559 -910 -7453 ... ## ..$ Std.Dev.Trade.PL : num [1:8] 5307 3082 2128 15350 1922 ... ## ..$ Percent.Positive : num [1:8] 66.7 33.3 33.3 66.7 25 ... ## ..$ Percent.Negative : num [1:8] 33.3 66.7 66.7 33.3 75 ... ## ..$ Profit.Factor : num [1:8] 12.195 1.865 2.458 37.72 0.535 ... ## ..$ Avg.Win.Trade : num [1:8] 7160 4625 2916 17157 1994 ... ## ..$ Med.Win.Trade : num [1:8] 7160 4625 1611 17157 1994 ... ## ..$ Avg.Losing.Trade : num [1:8] -1174 -1240 -593 -910 -1242 ... ## ..$ Med.Losing.Trade : num [1:8] -1174 -1079 -591 -910 -1192 ... ## ..$ Avg.Daily.PL : num [1:8] 4382 715 577 11134 -433 ... ## ..$ Med.Daily.PL : num [1:8] 4921 -970 -436 5894 -905 ... ## ..$ Std.Dev.Daily.PL : num [1:8] 5307 3082 2128 15350 1922 ... ## ..$ Ann.Sharpe : num [1:8] 13.11 3.68 4.3 11.51 -3.58 ... ## ..$ Max.Drawdown : num [1:8] -5505 -8591 -5372 -16197 -8023 ... ## ..$ Profit.To.Max.Draw: num [1:8] 2.512 0.836 1.01 2.054 -0.167 ... ## ..$ Avg.WinLoss.Ratio : num [1:8] 6.1 3.73 4.92 18.86 1.61 ... ## ..$ Med.WinLoss.Ratio : num [1:8] 6.1 4.29 2.73 18.86 1.67 ... ## ..$ Max.Equity : num [1:8] 17334 11288 7986 42611 2058 ... ## ..$ Min.Equity : num [1:8] -96.2 -2155.7 -2455.7 -701.2 -7623.2 ... ## ..$ End.Equity : num [1:8] 13829 7186 5425 33271 -1341 ...

There is an entry in results called tradeStats. This is a combined array of all trade statistics for all portfolios. I preview it below:

head(results$tradeStats)

## nFAST nSLOW Portfolio Symbol Num.Txns Num.Trades Net.Trading.PL ## 1 5 50 SMAC-20-50_PORTF.5 AAPL 61 30 2855.0673 ## 2 5 50 SMAC-20-50_PORTF.5 FB 39 19 11345.9006 ## 3 5 50 SMAC-20-50_PORTF.5 HPQ 37 18 7894.2676 ## 4 5 50 SMAC-20-50_PORTF.5 IBM 4 2 708.6119 ## 5 5 50 SMAC-20-50_PORTF.5 MSFT 65 32 2823.2581 ## 6 5 50 SMAC-20-50_PORTF.5 NFLX 45 22 28273.6792 ## Avg.Trade.PL Med.Trade.PL Largest.Winner Largest.Loser Gross.Profits ## 1 53.47184 -227.9242 2059.360 -968.2612 9048.215 ## 2 560.41601 -84.9241 8080.600 -1534.9605 17062.586 ## 3 273.62865 -210.1213 7138.418 -1353.8012 12826.443 ## 4 372.62668 372.6267 1268.772 -523.5185 1268.772 ## 5 63.63691 -184.3744 1846.308 -1215.2486 10221.590 ## 6 1286.11249 -139.8422 15127.305 -3202.4340 39031.541 ## Gross.Losses Std.Dev.Trade.PL Percent.Positive Percent.Negative ## 1 -7444.0601 747.8161 33.33333 66.66667 ## 2 -6414.6823 2139.0063 47.36842 52.63158 ## 3 -7901.1269 2080.1697 33.33333 66.66667 ## 4 -523.5185 1267.3407 50.00000 50.00000 ## 5 -8185.2090 777.3225 34.37500 65.62500 ## 6 -10737.0660 4016.0092 45.45455 54.54545 ## Profit.Factor Avg.Win.Trade Med.Win.Trade Avg.Losing.Trade ## 1 1.215495 904.8215 752.8397 -372.2030 ## 2 2.659927 1895.8429 908.8868 -641.4682 ## 3 1.623369 2137.7404 857.1655 -658.4272 ## 4 2.423547 1268.7719 1268.7719 -523.5185 ## 5 1.248788 929.2355 1059.7691 -389.7719 ## 6 3.635215 3903.1541 1987.2268 -894.7555 ## Med.Losing.Trade Avg.Daily.PL Med.Daily.PL Std.Dev.Daily.PL Ann.Sharpe ## 1 -310.2304 53.47184 -227.9242 747.8161 1.135091 ## 2 -493.6332 560.41601 -84.9241 2139.0063 4.159094 ## 3 -600.3886 273.62865 -210.1213 2080.1697 2.088157 ## 4 -523.5185 372.62668 372.6267 1267.3407 4.667462 ## 5 -366.3162 63.63691 -184.3744 777.3225 1.299595 ## 6 -694.1988 1286.11249 -139.8422 4016.0092 5.083754 ## Max.Drawdown Profit.To.Max.Draw Avg.WinLoss.Ratio Med.WinLoss.Ratio ## 1 -2921.3607 0.9773074 2.430989 2.426712 ## 2 -3311.4004 3.4263149 2.955474 1.841219 ## 3 -4740.7357 1.6651988 3.246738 1.427685 ## 4 -837.6125 0.8459901 2.423547 2.423547 ## 5 -2964.6203 0.9523169 2.384050 2.893045 ## 6 -7533.7804 3.7529205 4.362258 2.862619 ## Max.Equity Min.Equity End.Equity ## 1 4086.341 -1292.90199 2855.0673 ## 2 12361.105 -2716.54800 11345.9006 ## 3 7894.268 -4336.38823 7894.2676 ## 4 1343.862 -767.35374 708.6119 ## 5 2978.699 -2371.47934 2823.2581 ## 6 34903.375 -66.57307 28273.6792

Let’s see which combination did best. The last column of each tradeStats data frame in the list is End.Equity. It contains the total profit/loss for each stock tried in the portfolio. If we sum these we get the portfolio’s total profit/loss. Below I create a data frame containing the combination of parameters and their portfolio’s final profit.

library(dplyr)

(profit_dat <- results$tradeStats %>%

select(nFAST, nSLOW, Portfolio, End.Equity) %>%

group_by(Portfolio) %>%

summarize(Fast = mean(nFAST),

Delta = mean(nSLOW - nFAST),

Profit = sum(End.Equity)) %>%

select(Fast, Delta, Profit) %>%

arrange(desc(Profit)))

## # A tibble: 40 × 3 ## Fast Delta Profit ## <dbl> <dbl> <dbl> ## 1 20 105 99179.34 ## 2 5 120 93345.49 ## 3 5 70 88892.14 ## 4 15 85 86325.87 ## 5 10 115 83710.54 ## 6 50 75 82715.10 ## 7 40 85 81516.30 ## 8 30 70 80884.53 ## 9 30 20 80319.89 ## 10 40 35 76679.24 ## # ... with 30 more rows

plot(Profit ~ Fast, data = profit_dat, main = "Profit vs. Fast MA Window")

<!– –>

<!– –>

plot(Profit ~ I(Fast + Delta), data = profit_dat,

main = "Profit vs. Slow MA Window", xlab = "Slow")

Profit appears to be maximized with the fast moving average’s window is 20 days (4 weeks) and the slow moving average’s window is 125 days (25 weeks), which can be nicely interpreted as a monthly and a biannual period, respectively. With these periods, we manage to double the profit we had.

We have not searched the entire parameter space. One idea I’ve had to address this without actually trying every combination (a computationally intense task) is to fit a linear model to the profit, depending on the parameters of interest. I want to fit a model of the form:

Why this model? Convenience; if both

We will compute the least-squares fit with lm():

fit |t|) ## (Intercept) 75734.7811 7909.1511 9.576 2.6e-11 *** ## Fast -277.3674 493.5298 -0.562 0.5777 ## I(Fast^2) -0.8506 8.4920 -0.100 0.9208 ## Delta 162.8430 95.5322 1.705 0.0971 . ## I(Delta^2) -0.9096 0.3820 -2.381 0.0228 * ## --- ## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1 ## ## Residual standard error: 9548 on 35 degrees of freedom ## Multiple R-squared: 0.3694, Adjusted R-squared: 0.2974 ## F-statistic: 5.127 on 4 and 35 DF, p-value: 0.002334

Take partial derivatives of the above fit with respect to both

Whether this is a minimum or maximum depends on

Here we try out the optimized strategy.

strategy_st_opt <- "SMAC-1-90_Strat"

rm.strat(strategy_st_opt)

strategy(strategy_st_opt, store = TRUE)

add.indicator(strategy = strategy_st_opt, name = "SMA",

arguments = list(x = quote(Cl(mktdata)),

n = 5),

label = "fastMA")

add.indicator(strategy = strategy_st_opt, name = "SMA",

arguments = list(x = quote(Cl(mktdata)),

n = 95),

label = "slowMA")

add.signal(strategy = strategy_st_opt, name = "sigCrossover2", # Remember me?

arguments = list(columns = c("fastMA", "slowMA"),

relationship = "gt"),

label = "bull")

add.signal(strategy = strategy_st_opt, name = "sigCrossover2",

arguments = list(columns = c("fastMA", "slowMA"),

relationship = "lt"),

label = "bear")

add.rule(strategy = strategy_st_opt, name = "ruleSignal",

arguments = list(sigcol = "bull",

sigval = TRUE,

ordertype = "market",

orderside = "long",

replace = FALSE,

TxnFees = "fee",

prefer = "Open",

osFUN = osMaxDollarBatch,

maxSize = quote(floor(getEndEq(account_st,

Date = timestamp) * .1)),

tradeSize = quote(floor(getEndEq(account_st,

Date = timestamp) * .1)),

batchSize = 100),

type = "enter", path.dep = TRUE, label = "buy")

add.rule(strategy = strategy_st_opt, name = "ruleSignal",

arguments = list(sigcol = "bear",

sigval = TRUE,

orderqty = "all",

ordertype = "market",

orderside = "long",

replace = FALSE,

TxnFees = "fee",

prefer = "Open"),

type = "exit", path.dep = TRUE, label = "sell")

rm.strat(portfolio_st)

rm.strat(account_st)

initPortf(portfolio_st, symbols = symbols,

initDate = initDate, currency = "USD")

initAcct(account_st, portfolios = portfolio_st,

initDate = initDate, currency = "USD",

initEq = 100000)

initOrders(portfolio_st, store = TRUE)

# Retry the strategy

applyStrategy(strategy_st_opt, portfolios = portfolio_st)

updatePortf(portfolio_st)

dateRange <- time(getPortfolio(portfolio_st)$summary)[-1]

updateAcct(account_st, dateRange)

updateEndEq(account_st)

tStats <- tradeStats(Portfolios = portfolio_st, use="trades",

inclZeroDays = FALSE)

tStats[, 4:ncol(tStats)] <- round(tStats[, 4:ncol(tStats)], 2)

print(data.frame(t(tStats[, -c(1,2)])))

## AAPL FB HPQ MSFT NFLX NTDOY ## Num.Txns 26.00 22.00 29.00 35.00 17.00 33.00 ## Num.Trades 13.00 11.00 15.00 18.00 9.00 17.00 ## Net.Trading.PL 8302.25 12501.64 7699.08 2741.82 51860.00 -1497.25 ## Avg.Trade.PL 663.78 1163.36 540.86 178.38 5792.79 -61.12 ## Med.Trade.PL -122.34 -108.00 -53.17 -107.60 124.00 -615.00 ## Largest.Winner 4539.65 9949.11 5148.97 2901.77 41689.39 5538.01 ## Largest.Loser -579.22 -448.06 -1547.47 -566.57 -2344.88 -1045.17 ## Gross.Profits 10613.98 14085.00 13338.63 6965.03 56350.29 7150.00 ## Gross.Losses -1984.83 -1288.00 -5225.69 -3754.14 -4215.14 -8189.00 ## Std.Dev.Trade.PL 1501.47 2988.05 2012.72 898.07 14014.85 1563.62 ## Percent.Positive 46.15 45.45 33.33 33.33 55.56 11.76 ## Percent.Negative 53.85 54.55 66.67 66.67 44.44 88.24 ## Profit.Factor 5.35 10.94 2.55 1.86 13.37 0.87 ## Avg.Win.Trade 1769.00 2817.00 2667.73 1160.84 11270.06 3575.00 ## Med.Win.Trade 1260.55 1006.00 3443.84 818.41 3599.86 3575.00 ## Avg.Losing.Trade -283.55 -214.67 -522.57 -312.84 -1053.79 -545.93 ## Med.Losing.Trade -267.20 -175.00 -368.29 -340.92 -773.86 -660.00 ## Avg.Daily.PL 650.88 1149.36 319.06 149.59 6452.24 -178.16 ## Med.Daily.PL -135.14 -120.62 -108.87 -121.90 -117.48 -650.87 ## Std.Dev.Daily.PL 1500.18 2984.97 1913.27 922.20 14807.61 1552.16 ## Ann.Sharpe 6.89 6.11 2.65 2.57 6.92 -1.82 ## Max.Drawdown -1847.42 -4584.00 -3892.16 -3093.52 -9422.66 -7200.49 ## Profit.To.Max.Draw 4.49 2.73 1.98 0.89 5.50 -0.21 ## Avg.WinLoss.Ratio 6.24 13.12 5.11 3.71 10.69 6.55 ## Med.WinLoss.Ratio 4.72 5.75 9.35 2.40 4.65 5.42 ## Max.Equity 9150.73 14511.62 8123.84 5297.22 56502.52 2515.24 ## Min.Equity -63.46 0.00 -1656.13 -701.82 0.00 -6039.29 ## End.Equity 8302.25 12501.64 7699.08 2741.82 51860.00 -1497.25 ## SNY TWTR YHOO ## Num.Txns 44.00 7.00 41.00 ## Num.Trades 22.00 4.00 21.00 ## Net.Trading.PL 2613.26 1340.73 11957.32 ## Avg.Trade.PL 146.45 359.50 596.48 ## Med.Trade.PL -111.49 -499.00 -198.00 ## Largest.Winner 4123.32 0.00 11649.93 ## Largest.Loser -672.60 -1644.84 -935.19 ## Gross.Profits 6897.70 4068.00 18011.00 ## Gross.Losses -3675.80 -2630.00 -5485.00 ## Std.Dev.Trade.PL 961.31 2531.05 2697.18 ## Percent.Positive 36.36 25.00 38.10 ## Percent.Negative 63.64 75.00 61.90 ## Profit.Factor 1.88 1.55 3.28 ## Avg.Win.Trade 862.21 4068.00 2251.38 ## Med.Win.Trade 387.24 4068.00 603.00 ## Avg.Losing.Trade -262.56 -876.67 -421.92 ## Med.Losing.Trade -246.41 -612.00 -442.00 ## Avg.Daily.PL 132.54 -889.98 456.37 ## Med.Daily.PL -125.51 -625.56 -214.82 ## Std.Dev.Daily.PL 960.19 663.42 2700.19 ## Ann.Sharpe 2.19 -21.30 2.68 ## Max.Drawdown -3238.67 -5173.34 -4777.13 ## Profit.To.Max.Draw 0.81 0.26 2.50 ## Avg.WinLoss.Ratio 3.28 4.64 5.34 ## Med.WinLoss.Ratio 1.57 6.65 1.36 ## Max.Equity 5489.53 2146.08 13225.13 ## Min.Equity -442.19 -3027.27 -2146.87 ## End.Equity 2613.26 1340.73 11957.32

final_acct <- getAccount(account_st) plot(final_acct$summary$End.Eq["2010/2016"], main = "Portfolio Equity")

The results look promising. Let’s compare to the performance of SPY:

getSymbols("SPY", from = start, to = end, adjust = TRUE)

plot(final_acct$summary$End.Eq["2010/2016"] / 100000,

main = "Portfolio Equity", ylim = c(0.8, 2.5))

lines(SPY$SPY.Adjusted / SPY$SPY.Adjusted[[1]], col = "blue")

The strategy isn’t being beaten by SPY quite so badly as it was before, which is good news, and that’s after accounting for transaction costs (notice that we’ve kept those costs low; presumably we’ve found a very cheap brokerage service) and even a little slippage (that’s the 0.1% fee applied per transaction). So not bad. We can deploy this strategy and expect decent results.

Right?

Not so fast. We optimized the strategy using a data set, then evaluated its performance on the same data set. Any expert in statistics or econometrics or machine learning will protest this. Our approach may be leadng to overfitting, a phenomenon where a model describes the data it was trained on very well but does not generalize well to other data. I believe that my tactic of looking at a model obtained by maximizing a quadratic function may help combat this, but that’s just a hunch; we need to check the performance of the strategy on out-of-sample data (that is, data the strategy has never seen) in order to get a sense of how it would actually perform if deployed.

Notice that never did I look at stock data after October 2016, so why not see how the strategy would perform on more recent data?

start2 <- as.Date("2016-06-01")

end2 <- as.Date("2017-04-24")

getSymbols(Symbols = symbols, src = "yahoo", from = start2, to = end2,

adjust = TRUE)

stock(symbols, currency = "USD", multiplier = 1)

rm.strat(portfolio_st)

rm.strat(account_st)

initPortf(account_st, symbols = symbols,

initDate = initDate, currency = "USD")

initAcct(account_st, portfolios = account_st,

initDate = initDate, currency = "USD",

initEq = 100000)

initOrders(account_st, store = TRUE)

# Retry the strategy

applyStrategy(strategy_st_opt, portfolios = account_st)

updatePortf(account_st)

dateRange <- time(getPortfolio(account_st)$summary)[-1]

updateAcct(account_st, dateRange)

updateEndEq(account_st)

tStats <- tradeStats(Portfolios = account_st, use="trades",

inclZeroDays = FALSE)

tStats[, 4:ncol(tStats)] <- round(tStats[, 4:ncol(tStats)], 2)

print(data.frame(t(tStats[, -c(1,2)])))

## HPQ NTDOY SNY TWTR ## Num.Txns 3.00 3.00 3.00 6.00 ## Num.Trades 2.00 2.00 2.00 3.00 ## Net.Trading.PL 2404.89 -1070.06 687.21 -701.57 ## Avg.Trade.PL 1224.55 -514.50 363.00 -205.00 ## Med.Trade.PL 1224.55 -514.50 363.00 -140.00 ## Largest.Winner 491.99 0.00 0.00 0.00 ## Largest.Loser -14.84 -1599.88 -194.85 -454.30 ## Gross.Profits 2449.10 558.00 908.00 0.00 ## Gross.Losses 0.00 -1587.00 -182.00 -615.00 ## Std.Dev.Trade.PL 1014.30 1516.74 770.75 210.18 ## Percent.Positive 100.00 50.00 50.00 0.00 ## Percent.Negative 0.00 50.00 50.00 100.00 ## Profit.Factor NA 0.35 4.99 0.00 ## Avg.Win.Trade 1224.55 558.00 908.00 NaN ## Med.Win.Trade 1224.55 558.00 908.00 NA ## Avg.Losing.Trade NaN -1587.00 -182.00 -205.00 ## Med.Losing.Trade NA -1587.00 -182.00 -140.00 ## Avg.Daily.PL 491.99 -1599.88 -194.85 -219.33 ## Med.Daily.PL 491.99 -1599.88 -194.85 -154.35 ## Std.Dev.Daily.PL NA NA NA 210.16 ## Ann.Sharpe NA NA NA -16.57 ## Max.Drawdown -933.45 -1802.59 -694.00 -701.57 ## Profit.To.Max.Draw 2.58 -0.59 0.99 -1.00 ## Avg.WinLoss.Ratio NA 0.35 4.99 NaN ## Med.WinLoss.Ratio NA 0.35 4.99 NA ## Max.Equity 2542.89 153.54 999.21 0.00 ## Min.Equity 0.00 -1649.06 -337.03 -701.57 ## End.Equity 2404.89 -1070.06 687.21 -701.57

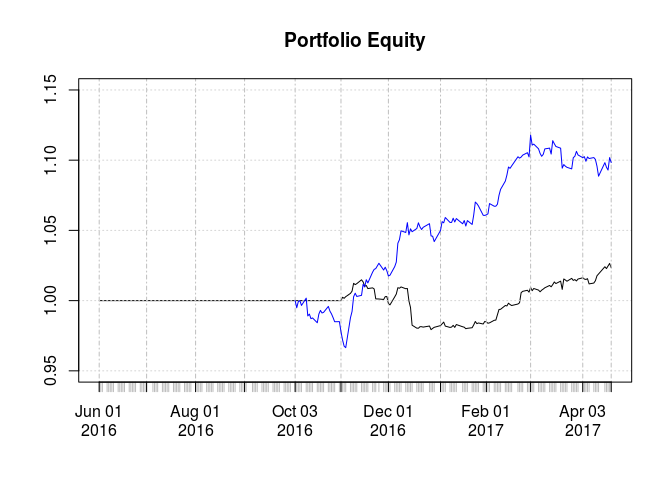

final_acct <- getAccount(account_st) plot(final_acct$summary$End.Eq["2016/2017"], main = "Portfolio Equity")

getSymbols("SPY", from = as.Date("2016-10-01"), to = end2, adjust = TRUE)

# I don't get quite as much SPY because our trading strategy has a warm-up

# period

plot(final_acct$summary$End.Eq["2016/2017"] / 100000,

main = "Portfolio Equity", ylim = c(0.95, 1.15))

lines(SPY$SPY.Adjusted / SPY$SPY.Adjusted[[1]], col = "blue")

Our strategy’s performance does not at all rival that of SPY out of sample. Admittedly, SPY’s behavior over this period is spectacular even by its own standards, with an annualized rate of return of about 21% (~10% is about normal), but the strategy has an annualized rate of return of about 5%, far below SPY’s “typical” performance.

Conclusion

If you were thinking about quitting your day job to day-trade full time, I hope I have curbed your expectations. Beating the market should be looking rather difficult by now.

I recently read an article on Bloomberg about why financial products always seem to burn investors. The article pointed the finger at p-hacking, backtesting without sufficiently checking out-of-sample performance, and overall sloppiness. This paragraph in particular jumped out at me:

The old adage applies: If asset managers and finance professors are super-smart, why ain’t they super-rich? The big money is being made by firms that ignore finance theory. Renaissance Technologies on Long Island is dripping with mathematicians and physicists but will not hire a finance Ph.D. Two Sigma Investments is run by computer scientists and mathematicians. D.E. Shaw was founded by a computational biologist. And so on. Reflecting mathematicians’ disdain for sloppiness in finance, a 2014 essay in the Notices of the American Mathematical Society referred to backtest overfitting as “pseudo-mathematics and financial charlatanism.”

quantstrat is a backtesting package. You need to backtest. Backtesting, though, is not nearly enough. You need to check out-of-sample performance, and even this must be done carefully lest you succumb to the same flaws of backtesting alone (that is, torturing the data until you get a confession).

In other words, we will need to look at some machine-learning techniques such as cross-validation to figure out what choice of parameters would be best. Packages such as caret may facilitate this, and I may look into them in the future. With that said, I doubt that the simple moving average crossover strategy will be very profitable, but that’s okay; I’ve been using it for pedagogical reasons only. With it, we’ve been able to see basically all of quantstrat‘s major features. We’ll keep using it as long as it’s useful.

Another great example – thanks. Wish this was around when i was trying to learn the quantstrat package!

One note i thought might be worth adding – i’ve had trouble with quantmod/quantstrat functions after loading dplyr/hadleyverse packages so have picked up the habit of unloading the package once its been used to continue working elsewhere with quantstrat. Haven’t run your code above to see if it still exists and perhaps it is fixed now but just thought i’d mention it if people where having issues running quantstrat the second time.

Sounds like I’m at a similar step in my own studies – moving from quantstrat backtesting to incorporate machine learning. Starting with some machine learning courses on datacamp/coursera to see what i can learn and then apply.

Will be interested to see what you post! Keep up the great work!

LikeLike

The Hadleyverse does NOT get along well with R/Finance. Reshape2 and ggplot2 may be fine. Beyond that, be very careful.

LikeLike

I have a question with calling getEndEq in one of the rule.

maxSize = quote(floor(getEndEq(account_st,

Date = timestamp) * .1)),

tradeSize = quote(floor(getEndEq(account_st,

Date = timestamp) * .1))

Not sure if this could get the update account end equity without calling updatePortf / updateEndEq.

Should it be inside the order side function and calling updateProf before calling getEndEq?

LikeLike

What you’ve caught is a hack I seemed to find. I wanted my trading system to base order size on the amount of equity in the portfolio. The above code seems to do that, looking up the equity available when placing an order. I remember reading through the source code of the relevant functions and my reading suggested the hack would work (and it seems to), so my answer would be: apparently not. This is intended to be run as the backtest is being performed, and I presume that you don’t need to update the portfolio there since the portfolio is already being run.

LikeLike

once again a very nice and interesting post! thanks a lot and I wish you will go on on that topic

LikeLiked by 1 person